Rising home prices upped the cost of housing. This trend was first gradual and then picked up momentum during the pandemic. Initially, low mortgage rates helped homebuyers absorb the shock of higher home prices, but as mortgage rates begin to rise, and are expected to continue to increase, housing affordability has become a chief concern. To help quantify the impact of shrinking affordability on homebuyer options, the research teams at ����ٴǰ�.���dz�® and the of Big gaming® used information from the Big gaming® Affordability Distribution Score and current inventory levels. The summarizes the findings.

The Double Trouble of the Housing Market Report Findings:

- More than 400,000 fewer affordable homes are available for sale for households earning $75,000 to $100,000 when compared to the start of the pandemic (245,300 in December 2021 vs. 656,200 in December 2019).

- For households earning $75,000 to $100,000, there’s one affordable listing available for every 65 households. That’s a sharp decline from one affordable listing for every 24 households in 2019 for this income group.

- Baltimore, Memphis, Birmingham, Detroit and St. Louis join five other metropolitan areas among the top 10 most affordable housing markets for Black households.

Nationwide Housing Affordability is Lower than Pre-Pandemic

Nationwide, housing affordability declined compared to pre-pandemic. Although mortgage rates are still lower than in 2019, home prices are more than 30% higher than then. On the other hand, wages rose 12% during the same time. As a result, the analysis found that:

– A household earning $75,000 to less than $100,000 can currently afford to buy 51% of the active housing inventory. Nevertheless, that same household could afford to buy 58% of the homes for sale in 2019. Thus, during the pandemic, affordability for households in the income bracket $75,000 to less than $100,000 dropped by 7%.

In the meantime, inventory plunged to a historic low during the pandemic. In fact, there is 57% less for-sale housing inventory than in 2019. While people can afford to buy fewer homes due to lower affordability, their options are even fewer since there are significantly fewer homes available for sale. Thus, the analysis also found out that:

– There are about 245,300 homes currently listed for sale that a household earning $75,000 to $100,000 can afford to buy. By comparison, there were 656,200 available homes for that same household pre-pandemic. Thus, due to the “double trouble”, there are nearly 411,000 fewer homes available for sale for this household compared to pre-pandemic.

And Household Growth Means More Competition for Limited Supply

When we compare the number of affordable listings with the number of households earning $75,000 to $100,000, we find the number of affordable listings per household. This is one way of assessing the supply against potential housing demand. It’s estimated that there are about 15.9 million households in the income bracket $75,000 to $100,000 but only 245,300 currently listed homes that they can afford to buy. This means that there is only one listing available for every 65 households of that income group. This is a stark decrease in availability from one listing for every 24 households in 2019.

In the affordability distribution curve shown below, which charts affordability by income in 2021 compared to 2019, we see how the “double trouble” impacted households in other income groups. The most impacted households are those earning $50,000 to less than $75,000. For this income group, affordability dropped by 6% while there are 63% fewer active listings that they can afford to buy. At the end of 2021, households earning $50,000 to $75,000 were able to afford nearly 165,280 listings compared to 450,220 at the end of 2019. With fewer homes in the entry level, the “double trouble” was expected to have a higher impact in the lower income levels. As income increases, the impact decreases.

Figure 1: Affordability By Income in 2021 vs. 2019

Lower Mortgage Rates and Higher Incomes Boost Affordability in Some Metros, but Low Inventory Erodes that Advantage

At a local level, it may be surprising to see that very expensive areas such as San Francisco, San Jose, Honolulu and Washington, DC are currently more affordable compared to pre-pandemic. How can these areas be more affordable? Home prices have increased but higher incomes coupled with lower mortgage rates seem to have eased affordability in these areas. For example, the income of the typical household rose by 15% in San Jose in the last 2 years. Respectively, the typical household income is 13% higher in San Francisco compared to 2019. Meanwhile, remember that in the first year of the pandemic, many people were leaving these big and expensive areas, so home prices were rising slower there compared to other areas during that time.

Even though households can afford to buy a greater share of homes, there are still fewer options for those households due to record low inventory. For instance, in San Francisco metro area, there are 180 fewer homes for a household earning $100,000 to $125,000 to buy. Compared to the number of households in this income group, there is an available listing for every 310 households. Nevertheless, there was a listing per 230 households in 2019. Respectively, there are about 300 fewer homes available for sale that a household in the income group $125,000 to $150,000 can afford to buy in San Francisco compared to pre-pandemic.

After comparing the number of affordable listings among the 100 largest metro areas, the National Association of Big gaming® and ����ٴǰ�.���dz�® were able to identify the top 10 areas with the most available homes for sale relative to the household population by income level. For instance, if your income is in the range of $75,000 to $100,000, , Deltona, FL, Des Moines, IA and Atlanta, GA are the top 3 areas for this income group with a listing per nearly 30 households.

See here the top 10 areas by income level and specifically how many listings are available for sale:

Top 10 Metros with Most and Least Homes for Sale per Household

Affordability Varies by Race and Ethnicity and Metro Area

There are sizable and persistent differences in the homeownership rate across racial groups. The homeownership rate for White Americans has been consistently near 70% since 2017. During the same period, the homeownership rate for Black Americans has been nearly 30 percentage points lower than those of White Americans near 40%. Thus, the National Association of Big gaming® and ����ٴǰ�.���dz�® also analyzed affordability by racial group to explain these variations on homeownership.

To do so, we created a score for each of the race groups that compares the share of households with the share of active listings that they can afford to buy in each income group. In balanced conditions, homes on the market are affordable to households in proportion to their income distribution. For example, a household in the 40th percentile of income should afford to buy 40% of the homes currently listed for sale. Thus, a score of 1 suggests a market in which the availability of homes for sale roughly matches the population’s ability to afford homes. A score of 2 means that all households can afford all of the homes that are currently on the market. Finally, a score of 0 shows that there isn’t any household in that specific income group that can afford any of the homes that are currently on the market. Thus, to put it simply, higher scores suggest better affordability conditions.

Nationwide, housing is more affordable for Asians among all other races as nearly 50% of them earn more than $100,000. In contrast, 35% of Whites, 25% of Hispanics and only 20% of Blacks have an income higher than $100,000. As a result, the housing affordability score for Whites is 0.86; 0.60 for Blacks; 0.70 for Hispanics and 1.03 for Asians. This means that Asians can afford a greater share of houses on the market than their income percentile. For instance, 51% of homes currently listed for sale are affordable to households with at least $100,000 in income. For Asian Americans, 48% earn more than $100,000 and can afford these homes, but for Black Americans, only 20% have the same level of affordability.

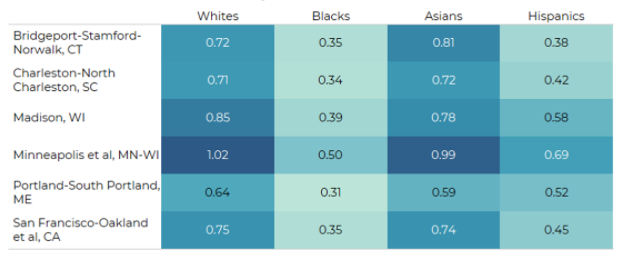

Since all real estate is local, these racial variations in affordability are even larger in some areas. Indeed, Bridgeport, CT, Charleston, SC, Madison, WI, Minneapolis, MN-WI, Portland, ME and San Francisco, CA were the areas with the biggest gap of affordability between White and Black households. In these areas, Blacks are half as likely to afford to buy a home than their White counterparts. For instance, in the San Francisco metro area, the affordability score for Whites is 0.75 compared to 0.35 for Blacks. Respectively, in Charleston metro area, the affordability score for Whites is 0.71 compared to 0.34 for Blacks.

Areas where Blacks are Half as Likely to Afford to Buy a Home Compared to Whites

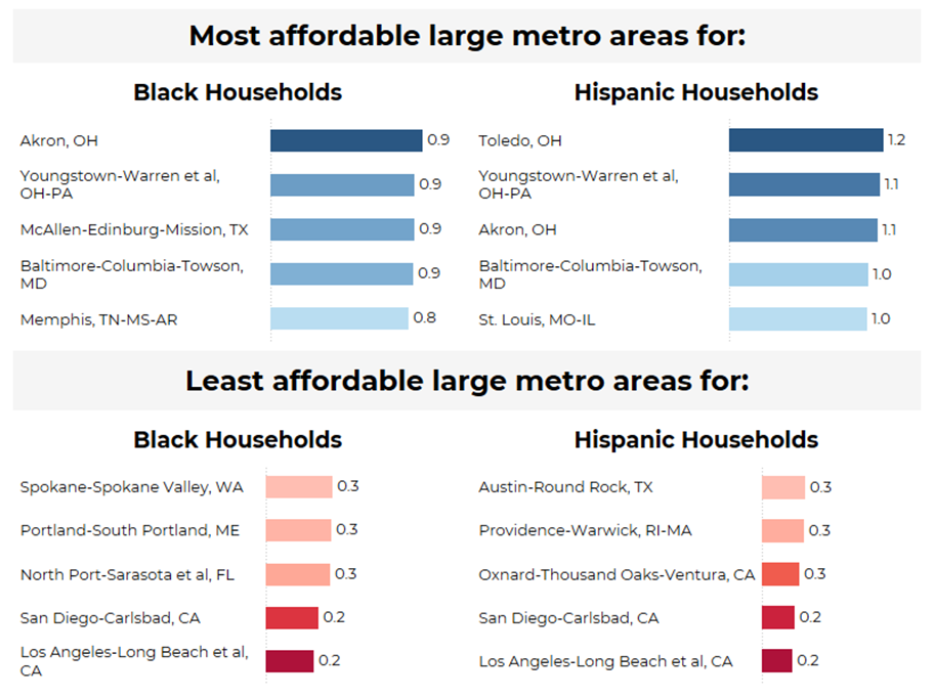

The current study also identified the most affordable areas by race. For instance, Akron, OH was the most affordable area for Black households with a score of 0.93. Some other affordable areas for Black households are: Youngstown, OH-PA, McAllen, TX, Baltimore, MD, Memphis, TN-MS-AR and Toledo, OH.

Most and Least Affordable Metro Areas for Blacks and Hispanics, By Affordability Score

*Methodology: The Big gaming® Affordability Distribution Curve and Score is a monthly NAR and ����ٴǰ�.���dz�® data series designed to examine affordability conditions at different income percentiles for all active inventory on the market. The Affordability Distribution Curve examines how many listings are affordable to those in a particular income percentile. The Affordability Score varies between zero and two and is a calculation that is equal to twice the area below the Affordability Distribution Curve on a graph. A score of one or higher generally suggests a market where homes for sale are more affordable to households in proportion to their income distribution.

Subscribe to our mailing list to receive monthly updates and notifications on the latest data and research.