We live in strange times for the economy and real estate markets. The year is dominated by the novel coronavirus, which continues to impact communities across the country. The pandemic led to a government-mandated shutdown of business activity that pushed the economy into a sudden and deep recession. The impact was felt immediately, with businesses furloughing or laying off millions of employees. The economic expansion of the 2010-19 period created 22.2 million jobs, and in just two months of quarantine—March and April of 2020—22.1 million jobs were wiped out. Some of the losses were recovered during the May through September months, which saw 11.4 million jobs added back to payrolls. However, as the impact from recession moved beyond the early casualties—airlines, hotels, conference venues, restaurants, bars and resorts—to touch a broader spectrum of companies, like retail, manufacturing and technology, the number of rising bankruptcies provided a clear signal that the employment recovery will take much longer than expected. The situation was underscored by July’s 10.2 percent headline unemployment rate, which was an improvement over April’s 14.7 percent, but remained above the rate of most historic recessions. The unemployment rate dropped further in September to 7.9 percent. However, with the number of workers permanently unemployed reaching close to 4.0 million as of September, the broader jobless rate is higher than the headline figure, and points to a long road ahead for the economy.

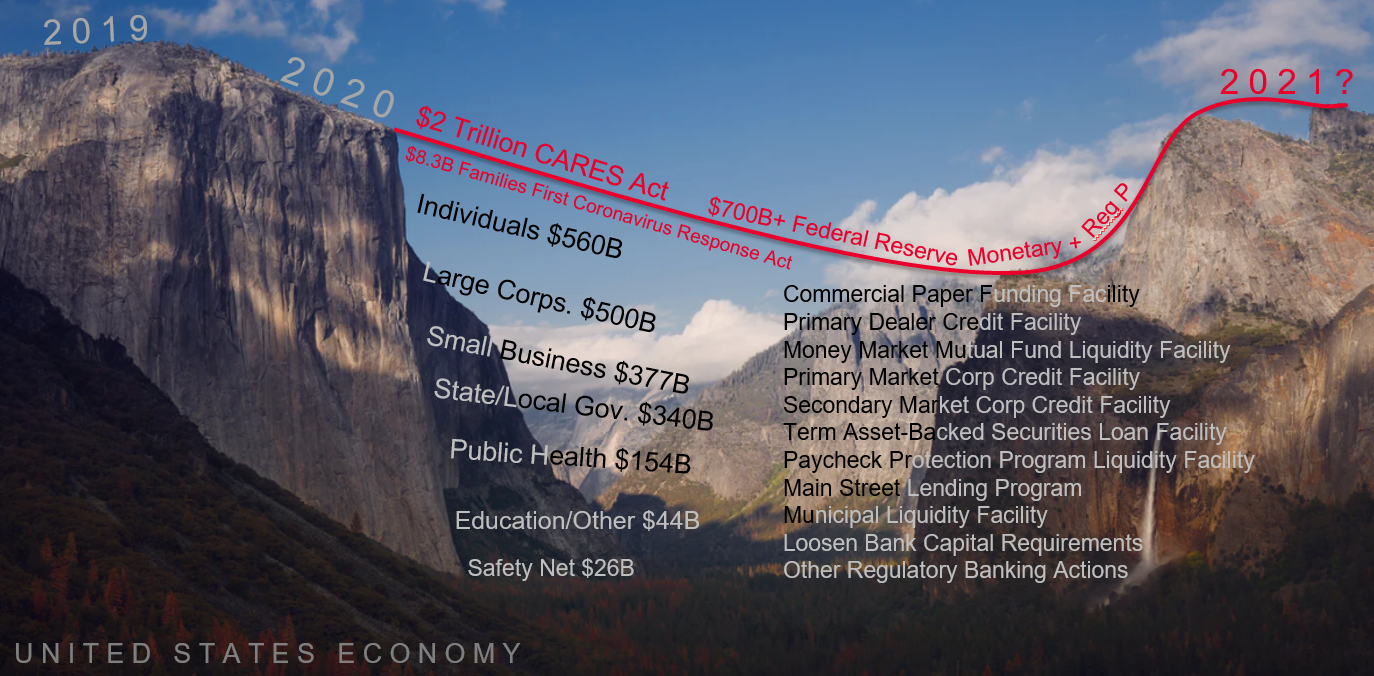

The silver lining of the current conundrum is the fact that monetary and policy makers recognized the deep chasm which opened beneath the virtual floor of the economy. The responses were significant and unprecedented, running from a return to zero interest rates and a host of monetary programs designed to ensure liquidity in the financial system, to an over $2 trillion legislative package aimed at building a figurative bridge across the chasm through enhanced unemployment benefits and foreclosure moratoria for workers, loans and grants to companies, and other regulatory measures. With an initial expectation that the pandemic would last about three months, these efforts rushed to ensure that the economy will regain solid footing at roughly the same level where it dropped off in mid-March.

Many of these initiatives proved successful at staving off an even larger wave of layoffs, and more importantly, a likely tsunami of evictions and foreclosures, akin to what we saw during the Great Recession. Simultaneously, companies across a wide range of industries recognized that web-centric technologies had advanced sufficiently to bring remote work fully into the mainstream. Almost overnight, millions of Americans found themselves working from home, able to maintain and enhance their productivity. This shift not only averted larger-scale job losses, but signaled a tectonic shift in real estate markets.

Freed by tech tools to work from anywhere, and concerned about continued health concerns from resurgent COVID cases, people have been seeking solutions to new-found problems—work from home, online schooling, social distancing—in real estate markets. Juiced by the Federal Reserve’s all-in quantitative easing, capital markets rode the “free money” train and rushed headlong into record-low interest rates for mortgage financing, further stimulating housing. Demand for homes accelerated after the quarantine period, with markets experiencing a frenzy similar to the booming 2000s, marked by offers made sight-unseen, multiple bids, price escalation clauses, and home inspection waivers. The surge in purchases came amid a significant shortage of supply, pushing prices higher at double the pace of the pre-pandemic period. The frothiness of housing markets mirrors that for other assets, like stocks and bonds, which have been reaching for new peaks, even as the overall economy remains sluggish and millions of Americans have lost both jobs and the enhanced unemployment benefits.

The discordance between hot real estate and stock markets and a slumping employment recovery casts a strange glow. Forbearance measures put in place to shield homeowners who have mortgages backed by government-sponsored enterprises (e.g. Freddie, Fannie) have successfully staved off foreclosures. At the same time, they also imprinted an artificial sense of security in markets’ health, and likely boosted valuations beyond levels warranted by existing economic concerns.

Just as importantly, policy measures aimed at preventing evictions and foreclosures merely postponed the recognition of loss or gain in the underlying financial contracts, which underpin millions of properties, both residential and commercial. For homeowners, there are two 180-day periods available to recover from any income losses and re-start payments to lenders. Effectively, this means that many struggling homeowners can skip payments until April of 2021, without fear of losing their homes. While this is a positive step over the short-term, it may also cause a delayed effect in the recognition of losses, should challenging economic conditions continue into 2021. As of the second quarter of 2020, mortgage delinquencies had already spiked to 8.22 percent of outstanding loans, reaching a nine year high, according to the Mortgage Bankers Association. The delinquency rate became more nuanced in the third quarter, as the share of early-stage delinquencies (less than 60 days) dropped, while the share of later-stage delinquencies increased.

For renters, the impact of eviction protection varies by state, and sometimes municipality. Some states had eviction protections in place until late August or September 1; others extended into early October. But as eviction protections in many states expired in September, the Centers for Disease Control and Prevention issued a temporary moratorium effective September 4 until December 31 of this year. These measures have staved off a large wave of housing losses for many tenants across the country. However, with a slowing recovery, many of these measures are likely to simply postpone the inevitable.

As we gaze across the chasm from partway across the figurative bridge, it is important to realize that we are not yet safely on the other side. Early third quarter data show promise that the economy continues to slowly heal, but persistent high unemployment, continued corporate bankruptcies and small business failures, along with flaring coronavirus cases should serve to temper the buzz induced by steeply rising real estate prices.